Quick Answer

The psychology of money explains why we spend based on feelings rather than logic. Stress, boredom, and social pressure push us toward purchases we later regret. Understanding your emotional triggers is the first and most important step to building better spending habits.

What You’ll Learn

- What Is the Psychology of Money?

- The Core Triggers Behind Emotional Spending

- Best Methods to Build Healthier Money Habits

- Step-by-Step: How to Break the Emotional Spending Cycle

- Common Mistakes Beginners Make

- Pro Tips for Long-Term Behavior Change

- Frequently Asked Questions

- Conclusion

The Spending Trap Nobody Warned You About

You just had a rough day. You open your phone, add a few things to your cart, and check out before you even realize what happened. Sound familiar?

That’s not a willpower problem. That’s the psychology of money at work. Our brains are wired to link spending with relief – and it happens fast, without much thinking involved.

A recent Bankrate survey found that nearly half of Americans (46%) consider emotional spending normal, and 38% say financial stress has made them spend even more. This pattern has a name: “doom spending.” And it’s more common than most people admit.

This guide breaks down exactly why emotional spending happens, what triggers it, and gives you a clear step-by-step plan to stop it from quietly draining your account – without making you feel guilty for being human.

What Is the Psychology of Money?

The psychology of money is the study of how emotions, mental shortcuts, and social pressure shape our financial decisions. Most people assume they make rational choices with money. Research consistently shows otherwise: feelings come first, logic follows.

Here’s why this matters: if you don’t understand why you spend, no budget will fix the problem for long. You might follow a plan for two weeks, fall off track, and wonder what went wrong. The issue usually isn’t the budget – it’s the behavior underneath it.

Three core concepts drive this field:

- Emotional spending – buying things to manage your mood rather than meet a real need. Stress, boredom, and sadness are the most common triggers.

- Cognitive biases – mental shortcuts that distort judgment. Seeing a product “on sale” makes it feel smart, even when the price is still high.

- Social influence – the quiet pressure to buy things because people around you have them, often without realizing it’s happening. This tension is especially real in relationships – if money conversations lead to arguments, our guide on talking about finances with your partner is worth reading alongside this one.

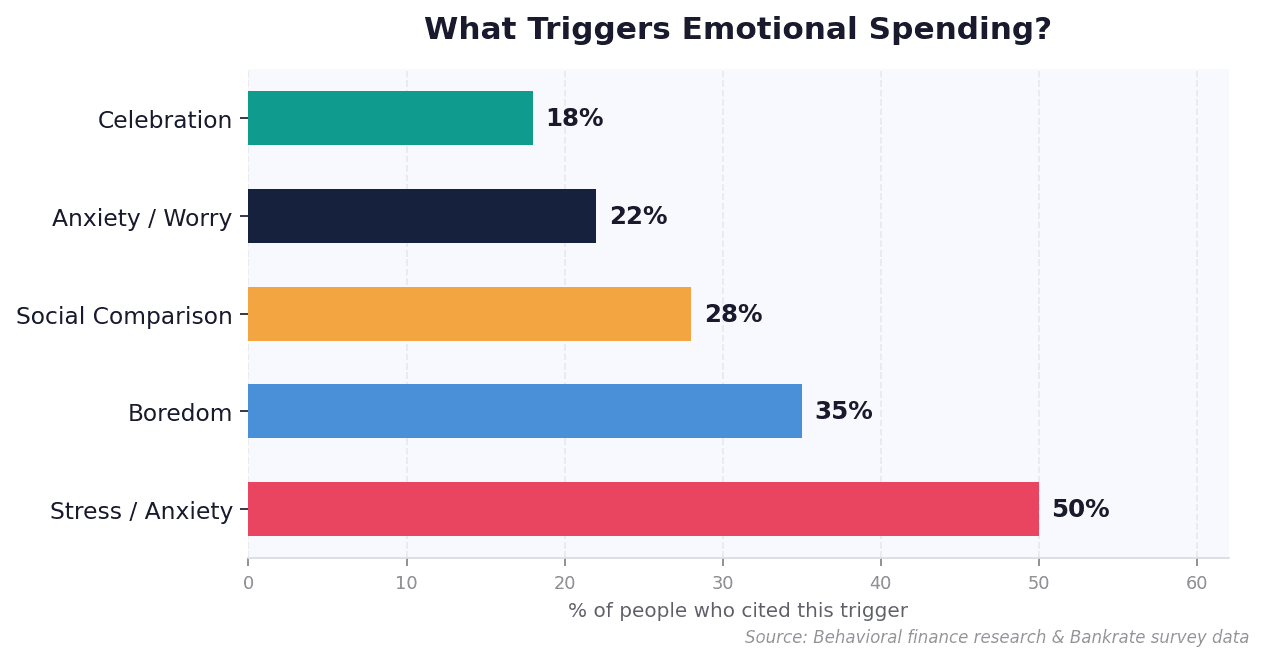

The Core Triggers Behind Emotional Spending

Knowing your triggers is half the battle. Once you recognize them, they lose some of their power.

- Stress and anxiety. When you’re overwhelmed, buying something new gives a short burst of relief. The relief lasts about 20 minutes — the credit card bill lasts a lot longer.

- Boredom. Scrolling through online stores has become a default time-killer. The purchase feels like it adds something to a dull moment. In reality, it just fills a few seconds.

- The anchoring effect. You see a jacket originally $200, now $90. Your brain locks onto the original price – so $90 feels like a win, even if you weren’t planning to spend $90 on a jacket.

- FOMO and scarcity tactics. “Only 3 left in stock.” “Sale ends tonight.” These are deliberate marketing moves designed to push you into deciding before you’ve had time to think.

- Social comparison. Seeing what others buy creates an urge to match it – mostly below the level of conscious awareness. Social media makes this worse on a near-daily basis.

Best Methods to Build Healthier Money Habits

These three methods work well for beginners because they’re practical and don’t require perfect discipline.

Values-Based Budgeting

Who it’s for: Anyone tired of feeling restricted by a budget

What it is: Instead of just cutting spending, you decide in advance what truly matters to you and put money there first.

Why it works: When your spending reflects your real values, cutting back in other areas feels less like punishment. The 50/30/20 budget rule is one of the cleanest frameworks to start with – it gives you structure without making every purchase feel like a negotiation.

The Spending Journal

Who it’s for: People who want to understand their patterns before trying to change them

What it is: A quick note after each purchase – what you bought, how much, and what you felt right before.

Why it works: Patterns show up fast. You can’t fix what you can’t see. Pairing a spending journal with one of the best free budgeting apps makes tracking nearly effortless.

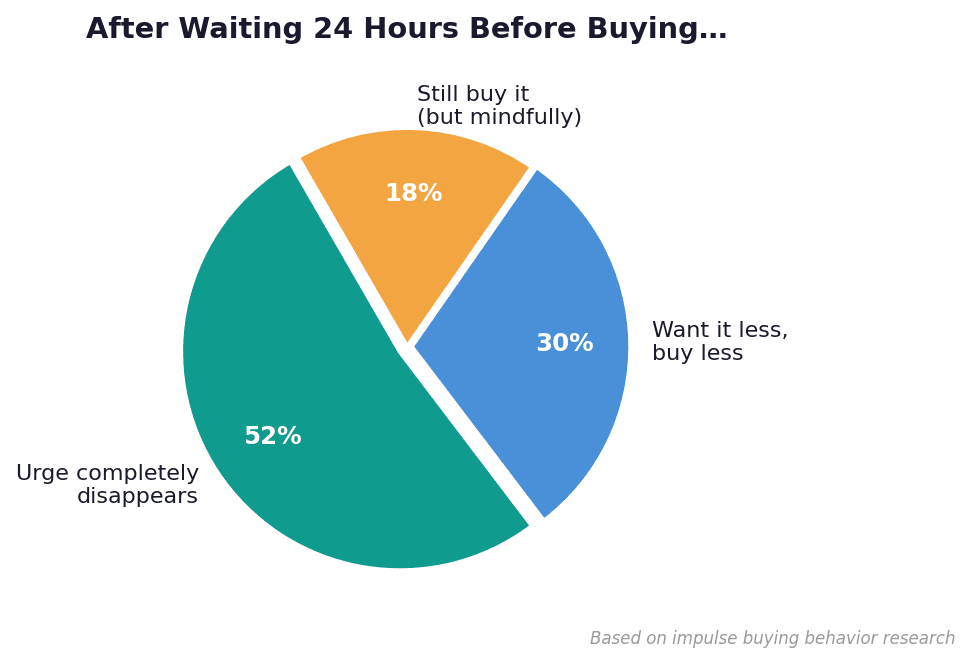

The 24-Hour Rule

Who it’s for: Impulse buyers and online shoppers

What it is: Before any unplanned purchase, you wait a full 24 hours.

Why it works: This single habit breaks the emotional loop. About half the time, the urge disappears before the 24 hours are up. Our full guide on how to stop impulse buying covers practical tactics to make this stick long-term.

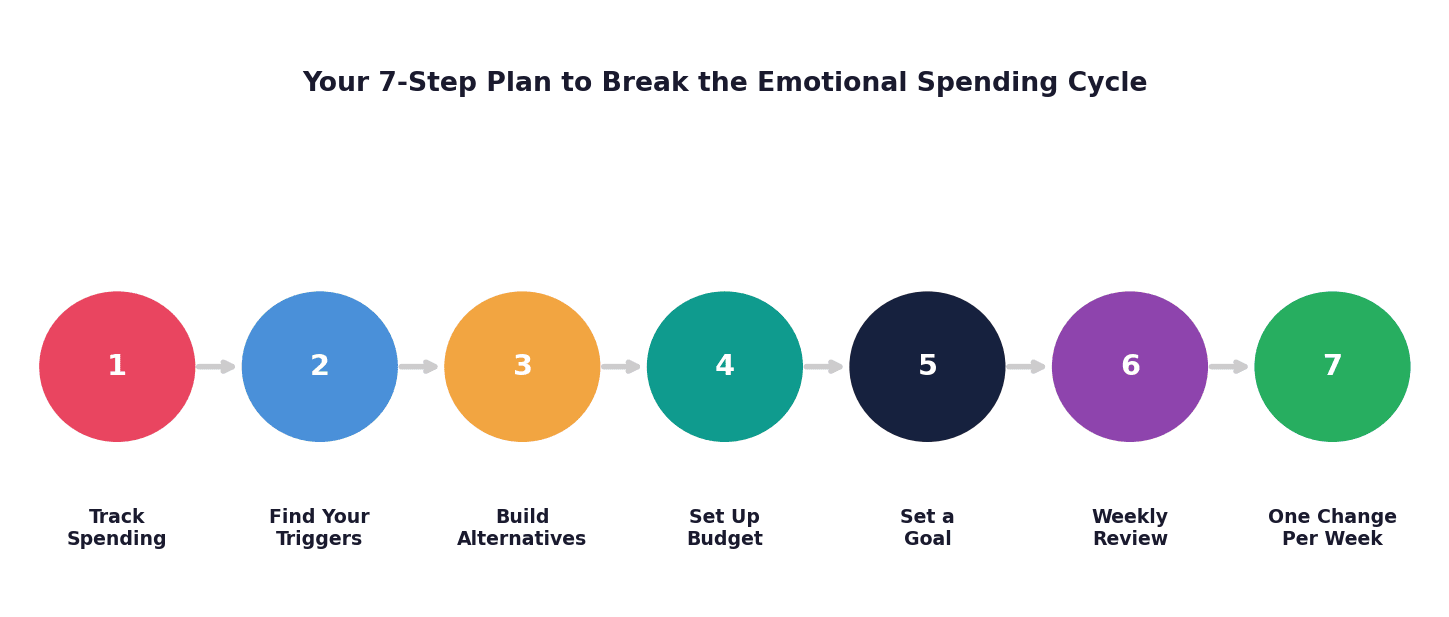

Step-by-Step: How to Break the Emotional Spending Cycle

Follow these steps in order. Don’t skip ahead – each one builds on the last.

- Track your spending for one week – no changes yet. Just observe. Write down every purchase and the emotion you felt right before it. You’re building awareness, not judging yourself.

- Identify your top two triggers. After a week, look back at your notes. Is the spending always after work? After scrolling? Most people have one or two consistent triggers, not ten.

- Create a non-spending alternative for each trigger. This step has to be specific. “I’ll do something else” doesn’t work. “I’ll go for a 15-minute walk after work” does. Decide in advance so you don’t have to think about it in the moment.

- Set up a simple budget. You don’t need anything complicated. A basic 50/30/20 split is a strong starting point. The 50/30/20 budgeting guide walks through this with real examples.

- Build one specific financial goal. “Save more money” is easy to ignore. “Save $500 in 60 days for an emergency fund” is something your brain can track. Use the financial goals checklist to map this out, and if you’re starting from zero, the guide on building your first emergency fund is the right place to begin.

- Review weekly – just 10 minutes. Compare what you spent vs. what you planned. No guilt – just data. Once a year, a bigger financial wellness check-up helps you see the bigger picture.

- Change one thing per week. Don’t try to fix everything at once. That’s how people burn out in week two. One small change per week, compounded over a few months, adds up to a completely different financial life.

Common Mistakes Beginners Make

These are the most common reasons people try to change their spending habits and give up:

- Trying to fix everything at once. Tackling all your triggers simultaneously leads to burnout fast. Pick one trigger, work on it for two weeks, then move to the next.

- Using restriction as the only strategy. “I’ll just stop spending” doesn’t work without a replacement behavior. If credit card debt is already part of the picture, this guide on paying off credit card debt gives you a concrete payoff plan to run alongside your behavior work.

- Ignoring your environment. If shopping apps are on your home screen and you get 20 promotional emails a day, the environment is working against you before the emotion even kicks in. Delete the apps. Unsubscribe from the lists. Pair this mindset with smart shopping hacks so saving feels like a win, not a sacrifice.

- Setting goals that are too vague. “Be better with money” gives your brain nothing to track. Specific, time-bound goals are the only kind that actually stick.

- Skipping the weekly review. You can’t improve what you don’t track. A 10-minute check-in is enough – you just have to stay honest with yourself.

Pro Tips for Long-Term Behavior Change

Small shifts that compound over time. None of these require radical discipline:

- Delay, don’t deny. Instead of “I can never buy this,” tell yourself you’ll buy it next month if you still want it. Most of the time, you won’t. This removes the feeling of deprivation that kills most budgets.

- Watch the numbers drop. Tapping a card is frictionless. Watching a balance go down in your banking app makes the cost feel real. Use whatever creates friction for you.

- Name the emotion out loud. Before clicking “buy,” say or write: “I’m feeling stressed.” This creates a pause in the automatic loop between emotion and action. That pause is where the choice lives.

- Think long-term, not just next month. Money you don’t spend impulsively can grow. Understanding how compound interest works changes how you think about every small purchase. And once you have a financial foundation, it’s worth exploring investing beyond just stocks to put your savings to work.

- Give yourself a guilt-free spending category. Budgets that allow zero fun never last. Allocate a small amount each month for anything you want – no justification needed. This makes every other category easier to stick to.

Frequently Asked Questions

What is emotional spending?

Emotional spending means buying something to manage a feeling like stress, boredom, or sadness rather than because you need it. It’s not a character flaw. It’s a very common response to how our brains handle negative emotions.

How do I stop impulse buying?

Start with the 24-hour rule. Before any unplanned purchase, wait a full day. Also identify the specific emotion that triggers the urge. Once you know your pattern, it’s much easier to interrupt it before the purchase happens.

Is budgeting enough to fix emotional spending?

A budget helps, but it’s not the complete answer. A budget gives you a plan. Addressing your emotional triggers is what makes you actually stick to the plan. Both are necessary and they work together, not separately.

How long does it take to change spending habits?

Most research points to 4–8 weeks to form a new habit with consistent effort. You’ll notice a difference within two weeks if you’re actively tracking and making small adjustments. Consistency beats perfection every time.

Does social media make emotional spending worse?

Yes, significantly. Constant exposure to what others are buying triggers social comparison and FOMO on a near-daily basis. Limiting social media or unfollowing accounts that trigger spending urges is one of the most practical steps you can take.

Conclusion

Here’s the honest takeaway: you’re not bad with money. You’re human.

The same brain that kept our ancestors alive is now reacting to Instagram ads and limited-time sales. It needs guidance – not punishment. Understanding the psychology of money doesn’t mean you’ll never make an emotional purchase again. It means you’ll start catching yourself, and over time, that awareness adds up to real, lasting financial change.

One action to take today: Open your last bank statement. Find one purchase driven by emotion, not need. Don’t judge it – just notice it. That noticing is where change starts.

Ready to keep building?

Start your budget with the 50/30/20 rule, map your goals with the financial goals checklist, and when you’re ready to grow your money, investing for beginners is a natural next step.

Leave a Reply