Disclosure: This post may contain affiliate links. If you buy through them, I earn a small commission at no extra cost to you. I only recommend tools I’d actually use.

Most people don’t realize they’re making money mistakes until the damage is already done. A missed savings habit here, a bad credit decision there — and suddenly you’re 35 wondering where the money went.

The good news? These mistakes are predictable. And because they’re predictable, you can stop them before they cost you thousands. This guide breaks down the five most damaging money mistakes beginners make — and gives you a concrete fix for each one.

In This Guide

Mistake 1

You Don’t Have a Budget – and You’re Guessing

I get it. Budgeting sounds boring. But here’s the thing: without one, you’re flying blind. You don’t actually know where your money goes each month. You just know it’s gone.

A budget isn’t a restriction. It’s a map. It shows you what you have, where it’s going, and what you can actually afford.

What it costs you

The average person who doesn’t track spending wastes $300–$500 a month on forgotten subscriptions, food delivery, and small daily purchases. That’s $3,600–$6,000 a year slipping out silently.

The fix

Start with the 50/30/20 rule: 50% on needs, 30% on wants, 20% on savings and debt. You don’t need to be perfect. You need to start. For a deeper walkthrough, read this beginner’s guide to budgeting.

Tool Recommendation

If you want a budgeting tool that actually changes your behavior — not just tracks spending — YNAB is worth it. Every dollar gets a job before you spend it. People who use it consistently report saving more in the first month than the app costs in a year.

Mistake 2

You Have No Emergency Fund

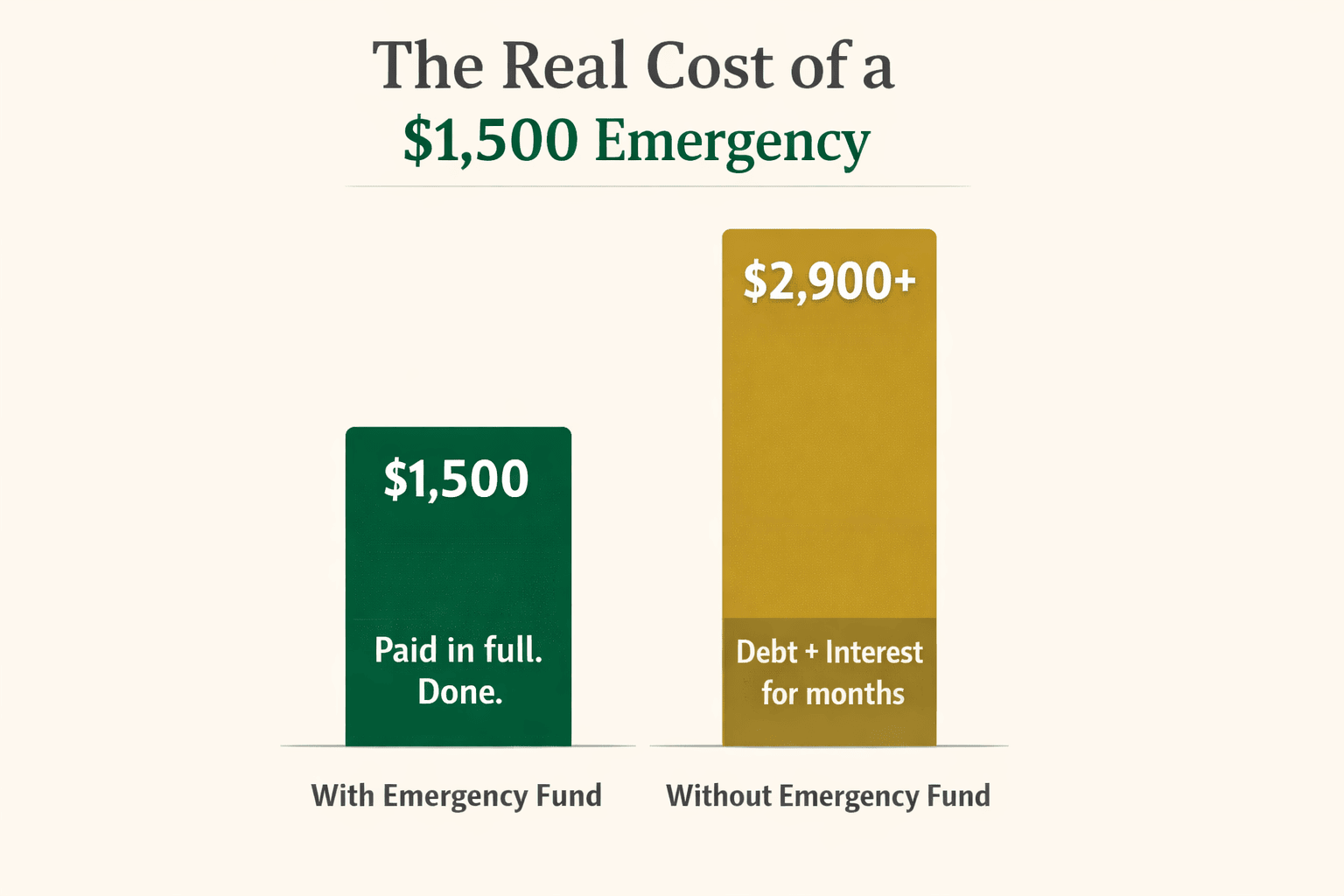

One unexpected bill and the whole plan collapses. No emergency fund means any crisis – car repair, medical bill, job loss – goes straight onto a credit card. You take on debt to survive the emergency. The debt accrues interest. You’re now behind before you even started.

What it costs you

A $1,500 emergency paid on a credit card at 22% APR, with minimum payments, can take years to clear and cost you nearly twice the original amount in interest.

The fix

Start with a $500 goal. Then $1,000. Keep it in a high-yield savings account — not your checking account where it’s too easy to spend. Read this step-by-step emergency fund guide to get started.

Mistake 3

You’re Only Paying the Credit Card Minimum

This one is sneaky. It feels responsible – you’re paying your bill, right? But the minimum payment is designed to keep you in debt as long as possible. The actual balance barely moves. Meanwhile, you’re charged interest every single month on the full amount.

What it costs you

A $3,000 balance at 22% APR, paid at minimum each month, can take over 10 years to clear and cost you more than $3,000 in interest alone. You’ll pay double what you borrowed.

The fix

Pay more than the minimum — even $50 extra a month makes a real difference. Use the avalanche method (highest interest first) to save the most money, or the snowball method (smallest balance first) for faster wins. Keep your total credit utilization under 30% of your limit.

Mistake 4

You’re Waiting Until You “Have More Money” to Invest

Every year you wait to invest is a year of compound interest you don’t get back. People think investing is for people with lots of money. It isn’t. It’s for people who want to build money.

What it costs you

Investing $100/month from age 22 to 65 at 7% average return gives you roughly $320,000. Wait until 32 and you end up with around $155,000. A 10-year delay cost you $165,000 — investing the same amount per month.

The fix

Start with whatever you have. Even $25 a month in a low-cost index fund beats doing nothing. Time is the only ingredient in investing that can’t be bought back.

Mistake 5

Your Spending Grows Every Time Your Income Does

This one has a name: lifestyle creep. You get a raise. You move into a bigger apartment. You upgrade your car. Your spending expands to match your income and you end up with the same savings as before, just with a fancier lifestyle.

What it costs you

Earn $5,000/month and spend $4,800 — you save $200. Get a raise to $6,000 and spend $5,800 — you still save $200. Your income grew by $1,000 and none of it built wealth.

The fix

When your income goes up, give every extra dollar a job before you spend it. Commit 50% of any raise to savings or investing first. For more tactics, read this post on stopping impulse buying.

Beginner money mistakes checklist

What People Get Wrong About These Mistakes

“I don’t earn enough to budget.”

A budget matters more on a tight income than a high one. That’s exactly where the savings hide.

“I’ll start investing once I’m out of debt.”

If your debt is low-interest (under 6%), invest at the same time. High-interest credit card debt is the exception — clear that first.

“I’ll wait until I know more.”

Waiting is the mistake. You learn personal finance by doing it imperfectly, adjusting, and doing it again.

Frequently Asked Questions

What are the most common money mistakes beginners make?

The five most damaging are: no budget, no emergency fund, paying only the credit card minimum, waiting too long to invest, and lifestyle creep. All five are fixable once you can see them clearly.

How do I start fixing my financial mistakes?

Start with one change, not five. Pick the mistake that costs you the most — usually no budget or no emergency fund — and fix that first. Small wins build the momentum you need for the rest.

How much money should I have in an emergency fund?

Financial experts recommend 3 to 6 months of essential expenses. If that feels impossible right now, start with $500. That covers most small emergencies and keeps them off your credit card.

What is lifestyle creep and why is it dangerous?

Lifestyle creep is when your spending rises in line with your income — so no matter how much more you earn, you never build more wealth. The fix is to save a portion of every raise before adjusting your spending.

Is it too late to start investing in my 30s?

No. Starting in your 30s is dramatically better than starting in your 40s or 50s. Even 25 to 30 years of consistent investing builds significant wealth. The best time to start was yesterday. The second best time is today.

Keep Reading

You Now Know What Most Beginners Don’t

These five mistakes aren’t complicated. But they’re easy to ignore — until they’ve cost you years of progress. Pick one from this list. Not all five. One. Fix it this week. That’s how financial habits actually form.

What’s the first step you’re going to take today? Drop it in the comments. Writing it down makes it real.

Want More Tips Like This?

Join the weekly newsletter. No spam — just simple money moves that work.

Leave a Reply