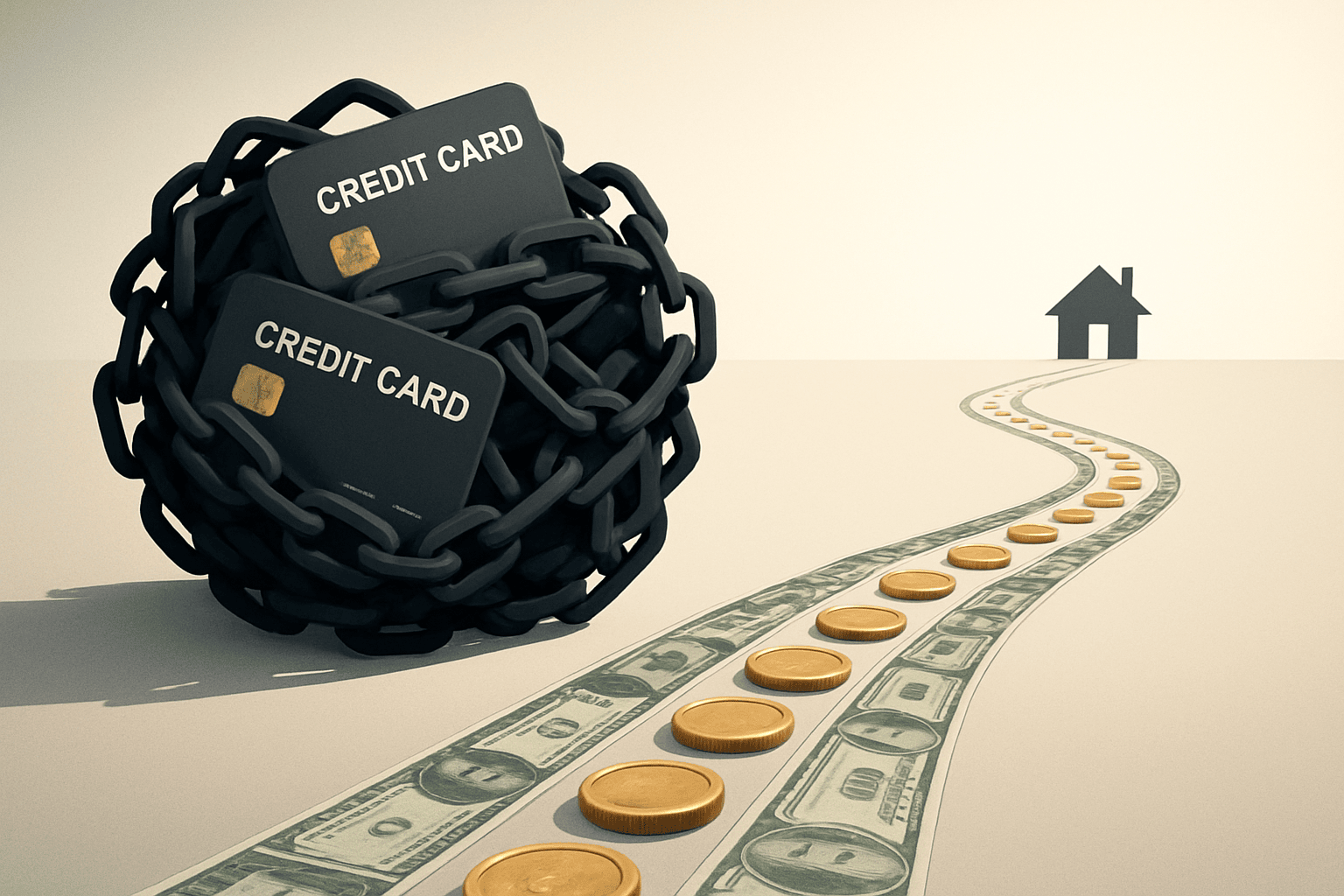

Credit card debt can feel overwhelming, but you are not alone. Millions of people feel trapped by mounting balances and endless minimum payments. This guide provides the essential knowledge and proven debt payoff strategies you need to break free and achieve debt-free living.

Phase 1: Understanding Your Enemy (The Debt)

The first step is a clear-eyed assessment of your financial situation.

Assess Your Debt

Gather all your credit card statements and create a simple list. For each card, note the outstanding balance, the minimum monthly payment, and, most importantly, the Annual Percentage Rate (APR). This simple act of organization transforms an overwhelming problem into a manageable task list.

The Power of the APR

The APR is the interest rate you pay on your balance. It is what keeps you on the debt treadmill. When you carry a balance, the interest charges can quickly negate your payments, especially on high-interest debt. For example, a card with a 25% APR will cost you significantly more over time than one with a 15% APR, even if the balances are the same. Understanding this difference is key to choosing the right payoff strategy.

Phase 2: Choosing Your Weapon (Debt Payoff Strategies)

There are two primary, highly effective strategies for tackling credit card debt. Both require commitment, but they appeal to different psychological needs.

Strategy 1: The Debt Snowball

The Debt Snowball method focuses on momentum. Here is how it works:

- List your debts from the smallest balance to the largest, ignoring the interest rate.

- Pay the minimum on all debts except the smallest one.

- Throw every extra dollar you can find at the smallest debt.

- Roll the payment from the first debt into the next smallest one once it is paid off.

This creates a “snowball” of increasing payments and provides quick, motivating wins. You can model this approach using a Debt Snowball Calculator

Strategy 2: The Debt Avalanche

The Debt Avalanche method is the mathematically superior choice. Here is how it works:

- List your debts from the highest APR to the lowest.

- Pay the minimum on all debts except the one with the highest interest rate.

- Direct all your extra funds to the highest-interest debt.

By eliminating the high-interest debt first, you save the most money on interest charges and shorten your overall payoff time. You can use a Debt Payoff Calculator to model your savings.

Using Balance Transfers Wisely

A balance transfer can be a powerful tool. This involves moving your high-interest debt from one card to a new card that offers a 0% introductory APR, often for 12 to 21 months. This gives you time to pay down the principal without accruing interest.

Tips for a Successful Balance Transfer:

- Check the Fee: Be aware of the balance transfer fee (typically 3-5% of the transferred amount).

- Set a Deadline: Make sure you can pay off the balance before the 0% period expires, or the new, higher rate will kick in.

Negotiation Tips

Do not be afraid to call your credit card issuer. Many companies would rather keep you as a customer. You can often negotiate a lower interest rate, especially if you have been a reliable customer.

How to Negotiate a Lower APR:

- Call the Number: Call the number on the back of your card.

- Be Polite: Politely ask to speak to someone about lowering your APR.

- Mention Your History: Highlight your good payment history, if applicable.

Phase 3: Real-Life Inspiration

Hearing how others have succeeded can provide the motivation you need to start your own journey.

Case Study: Sarah’s Snowball Success

Sarah, a single mother, felt overwhelmed by five different credit cards totaling $12,000 in debt. Her smallest balance was only $800. She chose the Debt Snowball method for the psychological boost. Paying off that first $800 in two months gave her the confidence to keep going. She quickly rolled that payment into the next smallest debt, and within 18 months, she was completely debt-free. She credits the early wins for keeping her motivated.

Case Study: Mark’s Avalanche Victory

Mark had $25,000 in debt spread across three cards. His largest balance, $15,000, also had the highest APR at 28%. He chose the Debt Avalanche method to save money. He focused intensely on that 28% card, cutting expenses and working extra hours. By eliminating the most expensive debt first, he saved thousands in interest. He paid off his entire high-interest debt load in just over two years. This proved the math-focused approach works.

Phase 4: Staying Debt-Free (Credit Card Management)

Paying off your debt is only half the battle. The real victory is achieving and maintaining debt-free living. This requires a fundamental shift in your approach to money.

Budgeting and Tracking

The foundation of debt-free living is a solid budget. Tracking every dollar helps you find spending leaks and redirect that money toward your debt or savings goals. For tips on cutting costs without feeling deprived, read our post on Smart Shopping Hacks. Effective credit card management means treating your card like a tool, not an extension of your income.

The Emergency Fund

One of the biggest reasons people fall back into credit card debt is an unexpected expense, such as a car repair or a medical bill. An emergency fund acts as a financial shield. Start small aim for $1,000. Then, work toward saving three to six months of living expenses. This fund will prevent a financial surprise from turning into a new debt crisis. If you need help getting started, we have a great guide: Build Your First Emergency Fund. For more in-depth guidance on budgeting and financial planning, consider picking up a copy of The Total Money Makeover.

Using Credit Cards Wisely

Once you are debt-free, the rule for credit card management is simple: never charge anything you cannot pay off in full when the statement arrives. Use your card for the rewards, but treat it like a debit card. If the money is not in your bank account, do not spend it.

Conclusion

Achieving debt-free living is a journey that requires discipline, but the reward is financial freedom. You now have the debt payoff strategies to tackle your credit card debt head-on.

Start your journey today. Share your favorite debt payoff strategies in the comments below. We are all in this together.

[…] Credit Card Debt: Your Guide to Pay It Off and Stay Debt-Free […]

[…] This is usually a credit card or a payday loan. If most of your balances are on credit cards, read Credit Card Debt: Your Guide to Pay It Off and Stay Debt-Free for a deeper […]

[…] without a replacement behavior. If credit card debt is already part of the picture, this guide on paying off credit card debt gives you a concrete payoff plan to run alongside your behavior […]