The Secret Life of Spouses

Imagine this: You’re scrolling through your bank statement, and a pit forms in your stomach. Not because of a big bill, but because you realize your partner has a secret credit card, a hidden debt, or a purchase they never mentioned. Sound dramatic? Unfortunately, it’s far more common than you think.

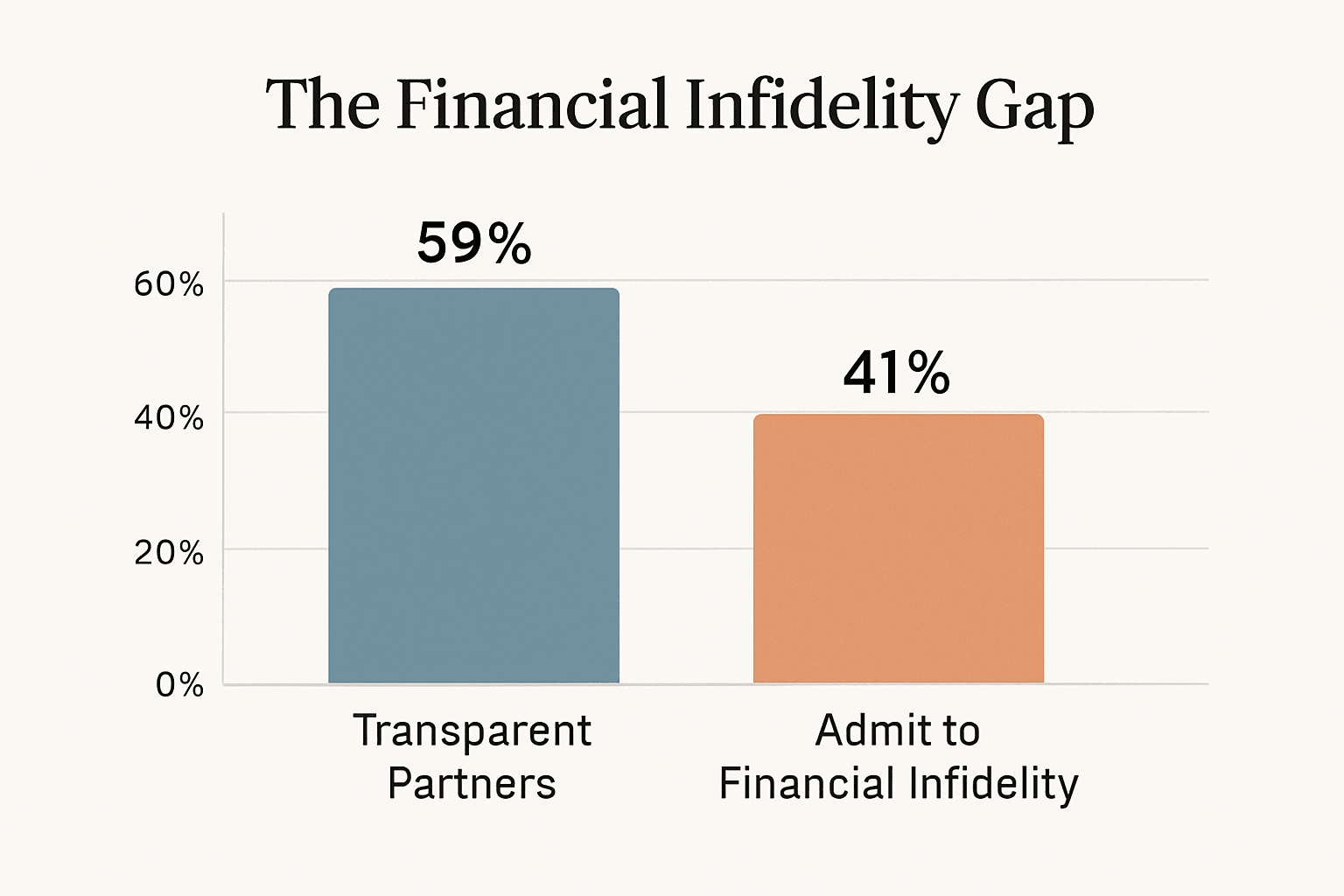

Here is the surprising statistic that highlights the significance of this issue in today’s world: A staggering 41% of American adults admit to committing “financial infidelity”—hiding accounts, debts, or spending habits from their spouse or partner. This isn’t just about a secret latte; it’s about a fundamental breakdown of trust.

This trend of financial secrecy is a symptom of a deeper problem: a lack of constructive, open communication about money. For many couples, money is the last taboo, the conversation that inevitably leads to raised voices and hurt feelings. In fact, money fights are often cited as the second leading cause of divorce, right behind infidelity .

But it doesn’t have to be this way.

We believe that achieving financial harmony with your partner is not about having the same income or the same spending habits; it’s about building a shared language and a safe space to discuss your finances. This article is your roadmap. We’ll provide practical advice, conversation starters, and a framework to transform money from a source of conflict into a tool for building a shared future.

The Roadmap to Financial Harmony

Talking about money is less about the numbers and more about the emotions, values, and history we bring to the table. Here are the essential steps to make your financial conversations constructive and calm.

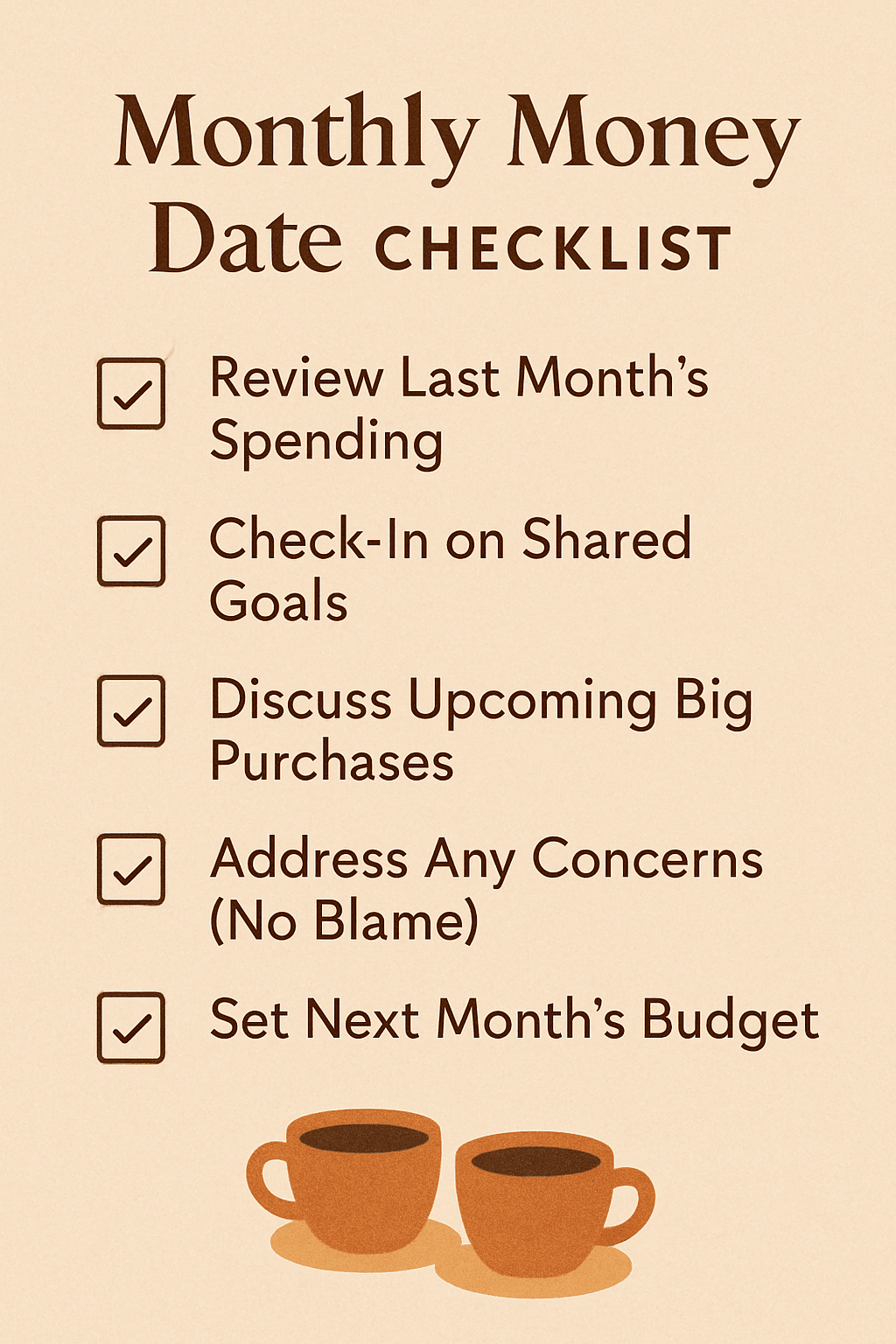

1. Schedule the “Money Date” (and Keep it Sacred)

The biggest mistake couples make is discussing money only when a crisis hits—like an unexpected bill or an overdraft notice. This immediately puts the conversation into a high-stress, reactive mode.

Instead, be proactive. Schedule a regular, non-negotiable Money Date. This should be a low-stakes, positive time, perhaps 30-60 minutes once a month. Crucially, it should not be a time for blame or judgment. Think of it as a business meeting for your family’s most important asset.

Conversation Starter: “I know talking about money can be tough, but I want us to be a team. Can we set aside 45 minutes every first Sunday of the month to check in on our finances? We can even order takeout.”

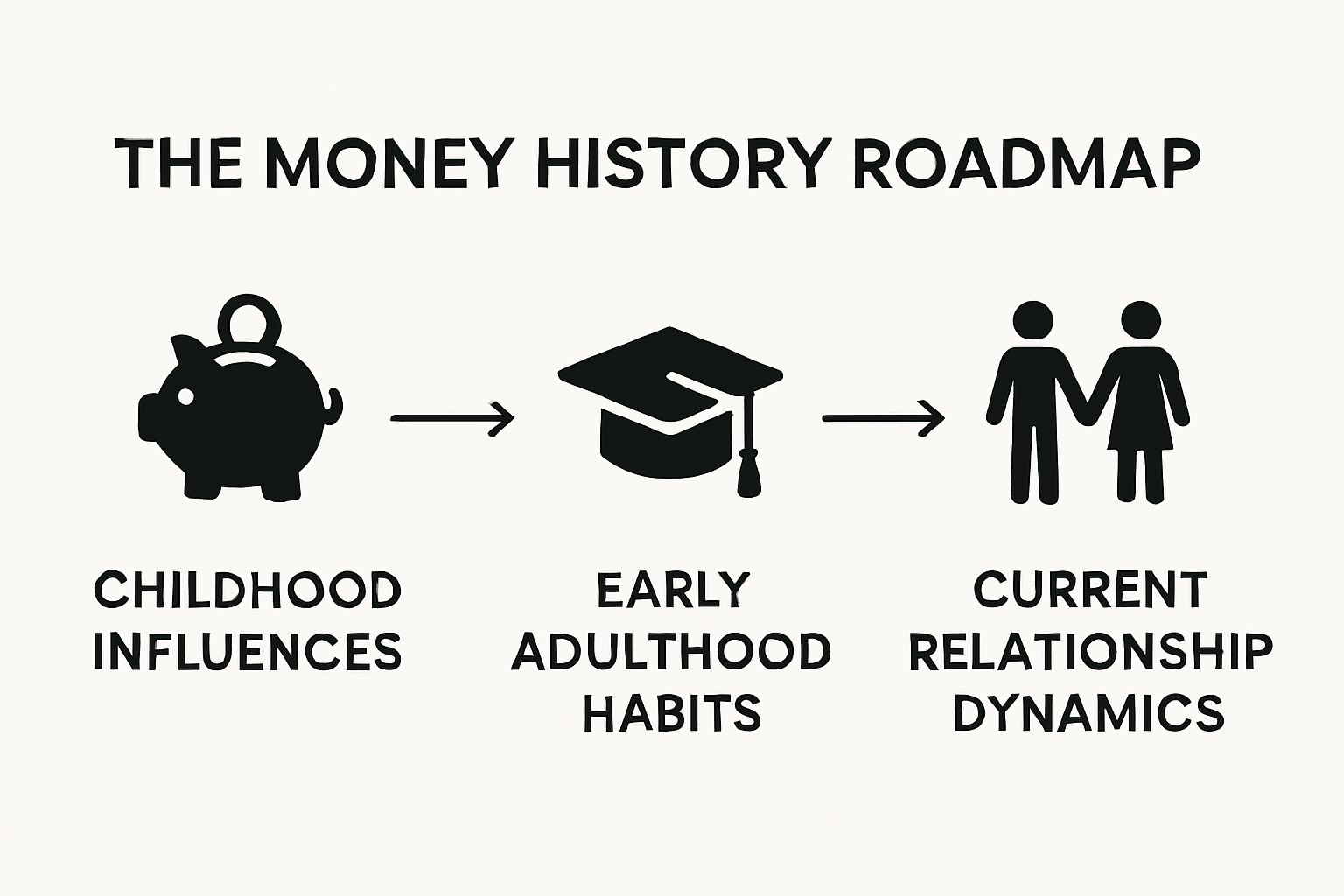

2. Understand Your Money History

Your partner’s current financial behavior is deeply rooted in their past. Did they grow up in a household where money was scarce, leading them to be a compulsive saver? Or was money never discussed, leading them to avoid the topic entirely?

Before you criticize a spending habit, take the time to understand the “why.” Discussing your childhood money habits can reveal profound insights into your current financial psychology.

Conversation Starter: “What is your earliest memory of money? What did your parents teach you about saving and spending?”

3. Define Your Financial Philosophy

Do you know what your partner’s biggest financial fear is? Or their biggest dream? Many couples skip the philosophical discussion and jump straight to the mechanics of joint accounts or who pays which bill.

Start by aligning on the big picture. This is where you can naturally transition into setting shared goals. If you need help structuring your ambitions, check out our guide on creating a Financial Goals Checklist.

Conversation Starter: “If we could achieve one major financial goal in the next five years, what would it be? Is it buying a house, starting a business, or being debt-free?”

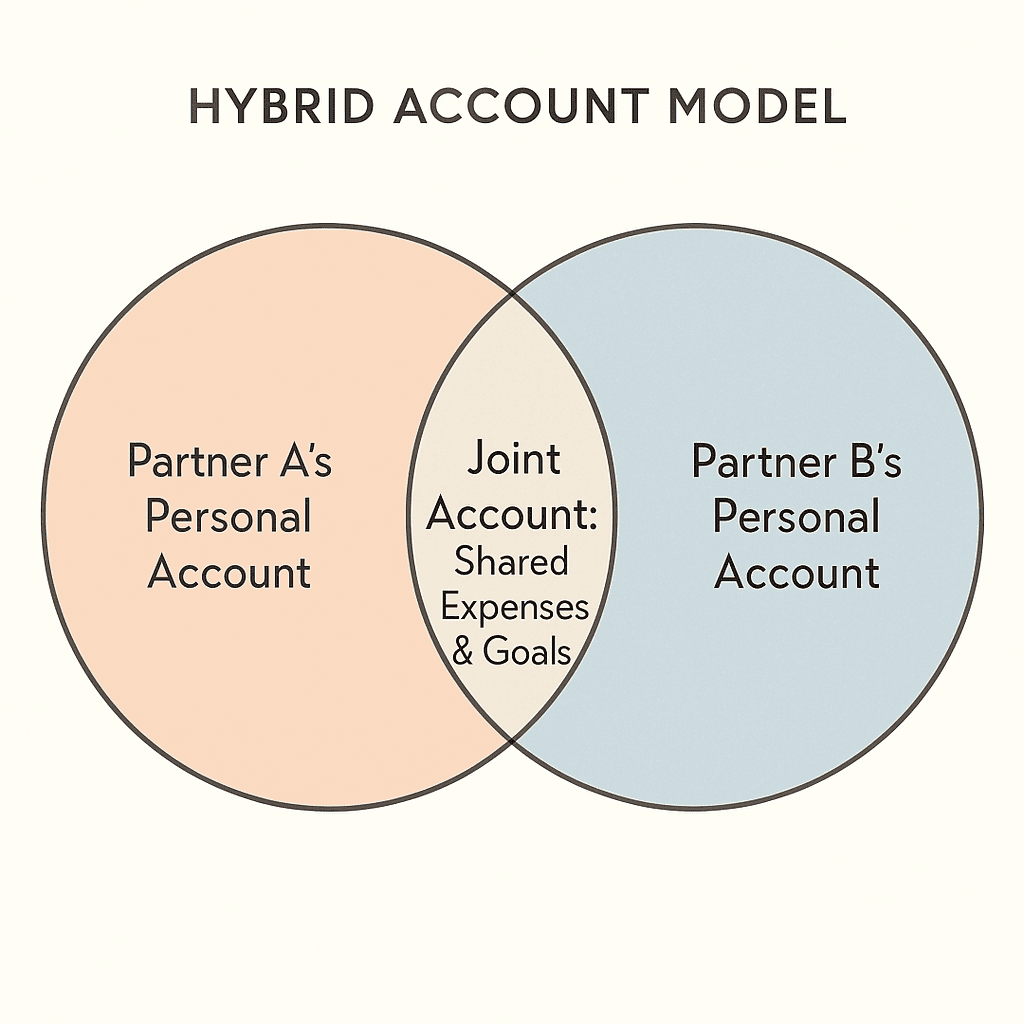

4. The Accounts Debate: Separate, Joint, or Hybrid?

The question of whether to merge finances is a major point of contention. There is no single right answer, but the most successful approach for many couples is the Hybrid Model.

| Account Type | Description | Pros | Cons |

| Joint | All income goes into one shared account. | Maximum transparency, simplified bill payment. | Loss of financial autonomy, potential for conflict over spending. |

| Separate | Each partner keeps their own accounts and pays specific bills. | Full autonomy, no need to justify personal spending. | Requires meticulous tracking, can feel less like a partnership. |

| Hybrid | A joint account for shared expenses/goals, and separate “fun money” accounts. | Balances teamwork with independence, fosters trust. | Requires more initial setup and agreement on contribution percentages. |

We recommend the Hybrid Model. You can agree to contribute a percentage of your income to the joint account for shared expenses (rent, groceries, utilities) and savings (like your Emergency Fund 101). The rest is yours to manage, no questions asked. This approach is a great way to start Budgeting for Beginners as a couple.

5. Create a Judgment-Free Budget

A budget is simply a plan for your money. It shouldn’t feel like a straitjacket. When creating one, focus on the future, not past mistakes. Use a simple framework like the 50/30/20 Rule to allocate funds for Needs, Wants, and Savings/Debt.

If you find yourselves arguing over the numbers, consider using one of the many excellent Free Budgeting Apps to keep the data neutral and objective.

Image Ideas to Support Understanding

These visuals are designed to clarify the concepts and make the advice actionable.

| Title | Alt Text | Description |

| The Financial Infidelity Gap | A bar chart showing that 41% of adults admit to hiding financial secrets from their partners, with the remaining 59% being transparent. | Supports the opening statistic and highlights the problem. |

| The Hybrid Account Model | A Venn diagram illustrating the overlap of two circles (Partner A’s Separate Account and Partner B’s Separate Account) with a third, larger circle in the center labeled “Joint Account for Shared Expenses & Goals.” | Clarifies the recommended account structure. |

| Monthly Money Date Checklist | A visual checklist with 5 items: 1. Review Last Month’s Spending, 2. Check-in on Shared Goals, 3. Discuss Upcoming Big Purchases, 4. Address Any Concerns (No Blame), 5. Set Next Month’s Budget. | Provides a practical tool for the “Money Date” step. |

| Money History Timeline | A simple timeline graphic showing three stages: Childhood Influences, Early Adulthood Habits, and Current Relationship Dynamics, with arrows connecting them. | Supports the “Understand Your Money History” section. |

Conclusive Summaries

We’ve covered a lot of ground, from the surprising prevalence of financial secrecy to the practical steps of setting up a Money Date and choosing a Hybrid Account Model. The most pivotal insight is this: Financial communication is a skill, not an innate talent. It requires practice, patience, and a commitment to approaching your partner with curiosity instead of criticism.

You now have the tools to start building a stronger, more transparent financial life together.

Your Challenge: We challenge you to apply one of the strategies from this post this week.

What is the one strategy you will commit to trying with your partner this week? Share your chosen strategy or results in the comments below!

A Short, Practical Takeaway

Financial harmony is built on communication, not just numbers.

One Simple Action

Schedule a 30-minute, judgment-free “Money Date” with your partner this week.

[…] is especially real in relationships – if money conversations lead to arguments, our guide on talking about finances with your partner is worth reading alongside this […]