I did the maths on a napkin in my first year in Abu Dhabi. Three months of rent, three months of everything else, done. I felt safe. Then a friend lost her job on a Sunday and had 30 days to either find new work or leave the country, and I realised my napkin maths had solved the wrong problem entirely.

An emergency fund for expats needs to cover more than monthly bills. Because losing your job abroad can also mean losing your visa, your health insurance, and your legal right to stay, the real target is closer to 6 to 9 months, split between a baseline living fund and a separate exit fund for flights, deposits, and the cost of starting over somewhere else.

Most of the advice out there was written for someone with a passport that matches their address. It assumes a family down the street, a government safety net, and a job that doesn’t come attached to your visa. None of that applies once you move abroad, and it’s exactly why the standard emergency fund number quietly fails expats.

In this guide:

- Why “Three to Six Months” Doesn’t Work for an Emergency Fund for Expats

- The Reframe: You Need Two Funds, Not One

- What Actually Puts an Expat’s Finances at Risk

- How Much to Actually Save in Your Emergency Fund for Expats

- Where to Keep an Emergency Fund for Expats

- How to Build It Without Wrecking Your Budget

- Frequently Asked Questions

Why “Three to Six Months” Doesn’t Work for an Emergency Fund for Expats

Every finance blog repeats the same rule: save three to six months of expenses. It’s not wrong, exactly. It’s just incomplete.

That number was built around a specific person. Someone who can move back in with parents if things fall apart. Someone whose health insurance isn’t tied to their employer. Someone who, worst case, files for unemployment and waits it out in the same city they’ve always lived in.

If you’re reading this from Dubai, Abu Dhabi, Singapore, or anywhere else you moved to for work, none of those safety nets exist for you. An emergency fund for expats has to do a completely different job than an emergency fund for someone who has never left their home country.

The Reframe: You Need Two Funds, Not One

Here’s the shift that changes everything: stop thinking of your emergency fund as one number. Think of it as two separate funds with two separate jobs.

The first is your baseline fund. This covers ordinary bad luck. A slow month, a medical bill, a broken laptop you actually need for work. This is the fund most generic advice is talking about.

The second is your exit fund. This covers the scenario nobody wants to plan for: losing the job that your visa, your housing, and your healthcare are all quietly attached to. This is the fund that generic advice never mentions, and it’s the one that actually protects you as an expat.

What Actually Puts an Expat’s Finances at Risk

Before you can size your emergency fund for expats correctly, it helps to see exactly why the risk is different. These aren’t hypothetical. They’re the specific ways a job loss abroad snowballs faster than it would back home.

Your Job and Your Visa Are the Same Thing

In the UAE, when your employment ends, your visa is cancelled too. You typically get a grace period of around 30 days to find new work or leave the country, though it can extend up to 180 days depending on your visa category and skill classification, according to Gulf News reporting on the current rules.

Thirty days is not a lot of runway to job hunt, pack a life, and make a decision, especially if your savings only cover ordinary expenses and nothing else.

There’s No Family Down the Street

Back home, a bad month sometimes means a free couch and a home-cooked meal while you sort things out. As an expat, there’s usually no one nearby to lean on. Any gap has to be covered entirely in cash.

You Might Be Supporting Two Households

A lot of expats send money home every month. If your income stops, that support doesn’t stop with it, at least not immediately. Your emergency fund needs to account for the fact that your monthly obligations may extend beyond your own rent and groceries.

Your Health Insurance Can Disappear With Your Job

In most expat setups, health insurance is provided by your employer. Lose the job, and you can lose coverage the same day, right when your stress levels and your risk of needing a doctor are both higher than usual.

How Much to Actually Save in Your Emergency Fund for Expats

Once you split the problem into two funds, the actual numbers get a lot clearer. This still starts from the standard rule the Consumer Financial Protection Bureau lays out for the general public. An emergency fund for expats simply adds a second layer on top of it.

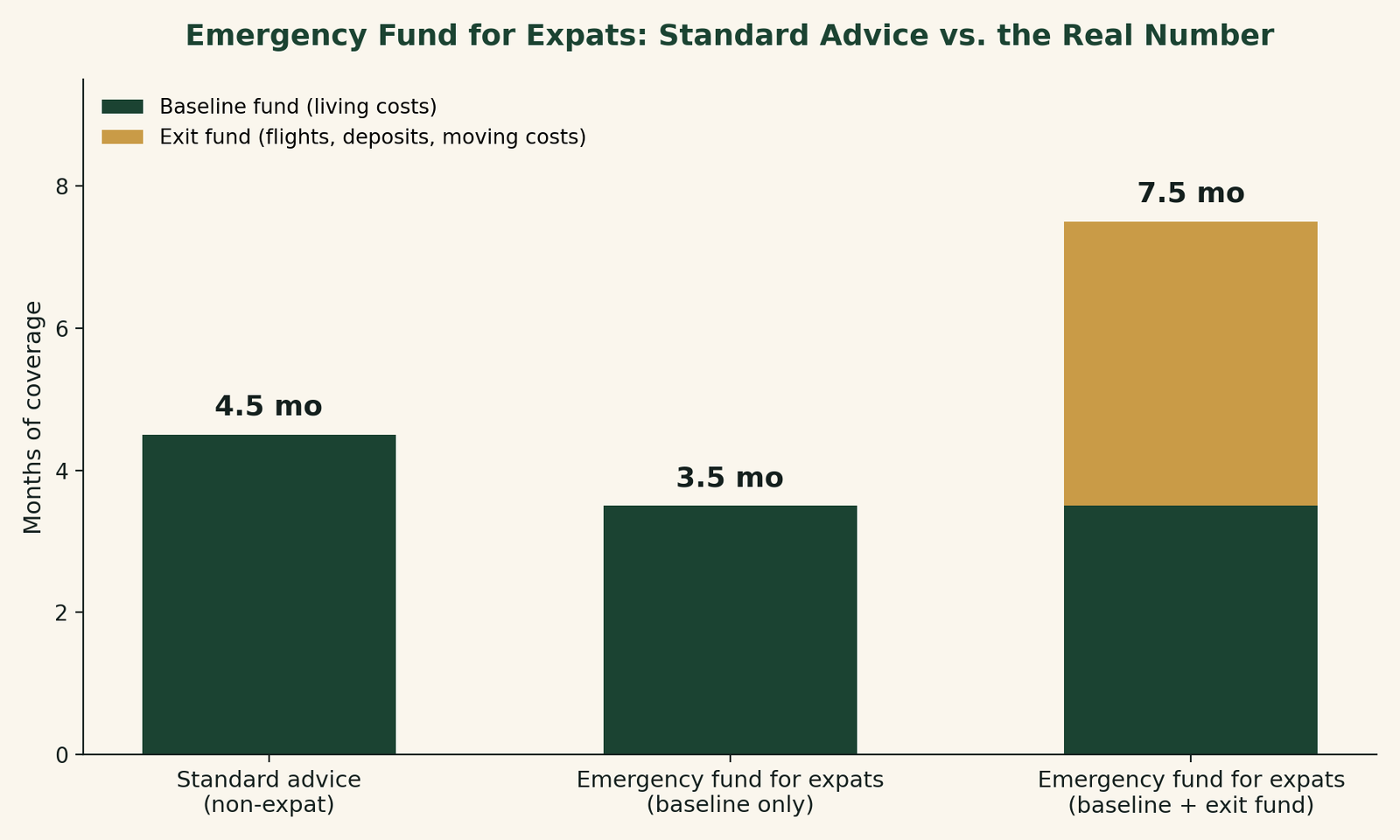

The Baseline Fund: 3 to 4 Months of Living Costs

This covers your normal monthly expenses if your income stops temporarily but your visa status isn’t the issue. Rent, food, transport, insurance premiums, and any fixed payments. If you already have a general savings habit, our Ultimate Beginner Emergency Fund Guide walks through building this baseline layer step by step, and it’s the right place to start if you haven’t built any cushion yet.

The Exit Fund: Your One-Way Ticket Out

This is the part most people skip, and it’s the part that actually matters for an emergency fund for expats. Price out, in USD, what it would genuinely cost you to leave on short notice: one flight home, a month of rent somewhere temporary, shipping or storing your belongings, and a buffer for the visa fees or agent costs involved in switching status.

For most people this lands somewhere between $2,000 and $6,000 depending on your home country and how much you’d need to move. Add that number on top of your baseline fund, and you land on a realistic 6 to 9 month target instead of the generic 3 to 6.

Where to Keep an Emergency Fund for Expats

An emergency fund only works if you can actually access it, in the right currency, fast. That rules out a few obvious places.

Don’t invest it. Money you might need in a genuine hurry has no business sitting in the stock market, where a bad week could force you to sell at the worst possible time. Our beginner investing checklist covers why this exact mistake trips up so many new investors, expat or not.

Split it instead across two things: a local account for day-to-day access, and a multi-currency account you can move from quickly if you need to send money home or pay for a flight in a different currency. This is one of the reasons I keep a Wise account alongside my local bank, since it lets me hold and convert USD and other major currencies without losing a chunk to conversion fees the moment I need the money.

How to Build It Without Wrecking Your Budget

Building a 6 to 9 month emergency fund for expats sounds intimidating written out like that. It doesn’t have to happen all at once. Here’s how I’d build an emergency fund for expats on a normal salary, one step at a time.

- Calculate your two numbers separately. Baseline monthly cost times 3 to 4, plus your one-time exit cost. Write both down.

- Automate a fixed transfer every payday. Even $200 a month builds real momentum over a year, and removing the decision removes the excuse.

- Track where the leaks are first. If you don’t already know where your money goes each month, our roundup of free spending tracker apps is a fast way to find the gap between what you earn and what you can actually save.

- Park it somewhere it can still earn a little. A zero-interest current account is a wasted opportunity. Look for a high-yield savings option, especially since local bank savings rates in the UAE are often close to zero.

- Rebuild immediately after you use it. Treat any dip back to zero as its own emergency. The fund only protects you if it’s actually full when you need it.

I’ve spent the past few months building CentsForward and freelancing on the side while still working a real estate job that isn’t where I want to be long term. It isn’t just ambition. It’s that I don’t want my visa, my income, and my sense of security all sitting on top of one employer. Building the exit fund forced me to say that out loud instead of just feeling it in the background.

None of this is about fear. It’s about not being the person who finds out, thirty days into a grace period, that the number on their napkin was solving the wrong problem.

If you haven’t started your baseline fund yet, that’s step one, and it takes about ten minutes to set the automation up today.

Frequently Asked Questions

How many months should an expat save in an emergency fund?

Most expats should target 6 to 9 months of coverage, split into a 3 to 4 month baseline fund for ordinary expenses and a separate exit fund of $2,000 to $6,000 for flights, deposits, and moving costs if a job loss also ends their visa.

What happens to my visa if I lose my job as an expat?

In the UAE, your employment visa is typically cancelled when your job ends, and you receive a grace period of around 30 days, extending up to 180 days for some visa categories, to find new work or leave the country. Always confirm your exact grace period through official government channels, since rules and durations can change.

Should I keep my emergency fund in USD or my host country’s currency?

A mix of both usually works best. Keep enough in your local currency to cover day-to-day bills without conversion fees, and hold the rest in USD or a multi-currency account so it’s ready to move quickly if you need to send money home or relocate on short notice.