I used to get paid and feel rich for about four days. Then the rent reminder would land, I’d send money home, cover a few things I didn’t even remember buying, and suddenly it was the 20th of the month and I was watching my balance like it owed me an explanation.

If you are trying to figure out how to budget on an expat salary, that feeling is familiar. It is one of the most common frustrations among expats earning good money but never actually getting ahead.

It is not about earning too little. I know people earning $2,000 who save more than people earning $6,000. The problem is not the salary. The problem is the absence of a system designed for how expat life actually works.

Every guide you find talks about 401ks, Roth IRAs, and local credit unions. None of that applies to you. This post will show you exactly how to budget on an expat salary — without feeling like you are giving up the life you moved abroad for.

The Short Answer

To budget on an expat salary without feeling restricted, assign every dollar a role the day it arrives, automate savings before your brain starts spending, and build your system around expat realities like remittances, currency risk, and the absence of a local pension. The method below works whether you earn $3,000 or $9,000 a month.

In this guide:

- Why Expat Budgets Fail Before February

- The Reframe That Changes Everything

- Step 1: Find Your Real Take-Home Number

- Step 2: Map Your Fixed Expat Costs First

- Step 3: Apply the 50/30/20 Rule — Expat Version

- Step 4: Automate Before You Think

- Step 5: Budget Your Remittances Like Rent

- Step 6: Build a Guilt-Free Spending Category

- Step 7: Review Monthly, Adjust Quarterly

- The Tools That Make This Stick

- Frequently Asked Questions

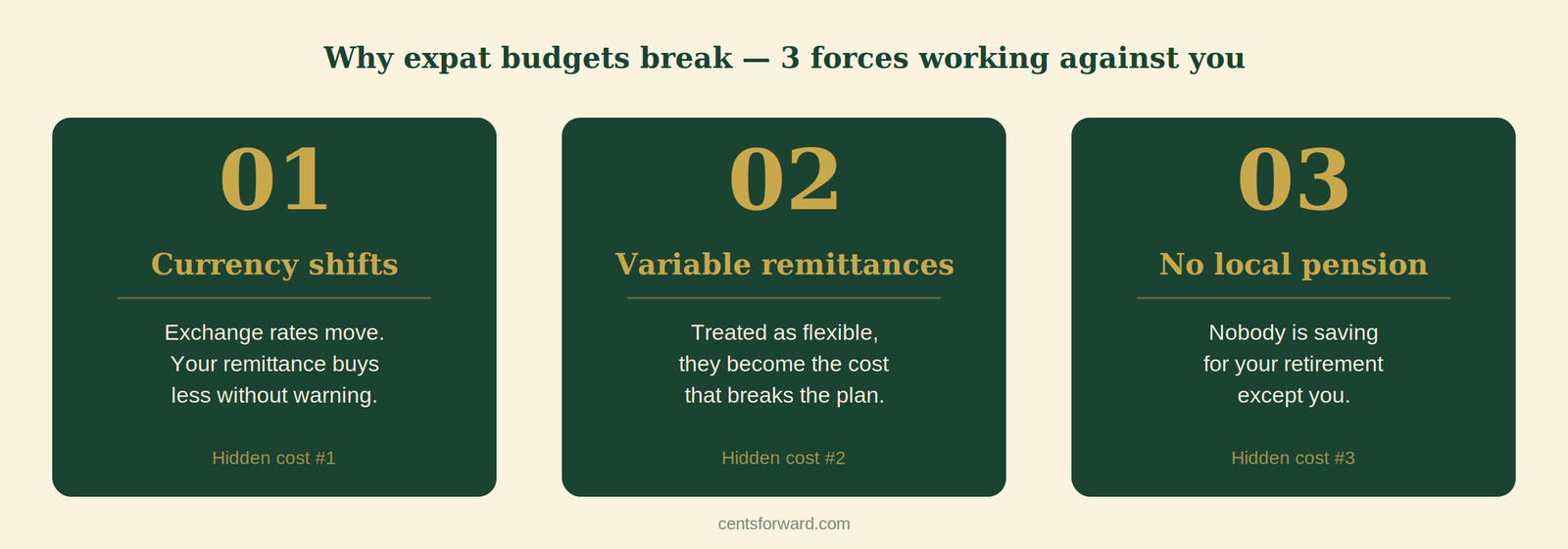

Why Expat Budgets Fail Before February

January always feels like a fresh start. You write down your income, your rent, your expenses. On paper it balances.

Then February arrives and something breaks the plan. An unplanned flight home. A friend visiting. An exchange rate that moved while you were not paying attention and quietly took $200 from your remittance.

Most budgeting systems are built for stable, predictable lives in a single currency. Expat life is not that.

When you are working out how to budget on an expat salary, you are dealing with at least three things most budgeting advice completely ignores: currency risk, cross-border obligations, and the absence of a local pension.

Generic advice was not built for that combination. The failure is not you. It is the mismatch between your actual financial life and advice that was never written for it. That is exactly why knowing how to budget on an expat salary requires a different approach entirely.

The Reframe That Changes Everything

Most people treat a budget like a diet. Restriction. Sacrifice. White-knuckling through the end of the month.

That framing is exactly why budgets collapse.

Think about it differently. Your salary is raw material. A carpenter does not feel restricted by wood — they shape it into something intentional.

Your budget is the blueprint. The money is the material. Feeling restricted simply means you have not decided what you are building yet.

The moment you connect how you budget on an expat salary to a specific goal — an investment account, a year without financial panic, the ability to say no to a job you hate — restriction becomes direction.

This is the psychology behind every system that actually works. It is not discipline. It is clarity. The psychology of money post on CentsForward goes deeper on exactly this.

Step 1: Find Your Real Take-Home Number

This sounds obvious. It rarely is.

Most people know their gross salary. Very few know the number that reliably lands in their account every single month after everything is accounted for.

Write down every fixed monthly inflow: your base salary, any housing allowance paid as cash, any transport stipend paid in cash. Add those together. That is your working number.

Do not build your budget around your annual salary divided by 12. Bonuses are not guaranteed. Annual leave payouts are not guaranteed. Build on what is certain.

Anything above that is extra, and it gets allocated separately when it arrives.

Expat Note

If your employer pays your rent directly to a landlord, do not count it as income or as an expense. Budget only what flows through your hands. Many expats mentally inflate their income by including perks they never receive as cash, then wonder why the numbers never add up.

Step 2: Map Your Fixed Expat Costs First

Fixed costs exist whether you leave the house or not. For expats, these are typically higher than for locals and carry dimensions that standard budgeting guides never mention.

Write every fixed cost in USD, even if you pay in a local currency. This forces you to confront exchange rate exposure, which is often the most invisible drain on expat finances.

| Fixed Cost Category | Expat-Specific Note |

|---|---|

| Rent | Often paid annually in the UAE. Divide by 12 and treat as monthly. |

| Health insurance | Confirm whether employer cover includes repatriation and home country visits. |

| Remittances home | Budget this as a fixed cost, not a flexible one. More on this in Step 5. |

| Savings and investments | Treat this like a bill you pay yourself. The most important line on the list. |

| Visa and renewal fees | Annualise and divide by 12. Catch this before it catches you. |

When you see all of this written down together, your real fixed commitments are almost always higher than you assumed.

That clarity, uncomfortable as it is, is exactly what you need before you can learn how to budget on an expat salary in a way that actually sticks.

Step 3: Apply the 50/30/20 Rule — Expat Version

The 50/30/20 rule is one of the most useful starting points when you are working out how to budget on an expat salary.

In its standard form: 50% to needs, 30% to wants, 20% to savings. Simple enough. But the expat version needs one meaningful adjustment.

You have no employer pension, no tax-advantaged retirement account, and no government safety net accruing in your host country. Your savings rate needs to carry more weight than 20%.

- 50% to needs: Rent, utilities, food, transport, insurance, remittances

- 20% to wants: Travel, restaurants, hobbies, subscriptions, social spending

- 30% to your future: Emergency fund, investments, gratuity planning

That 30% is not aggressive. For an expat with no local pension building in the background, it is the minimum that makes the math work long-term.

If 30% feels impossible right now, start at 20% and build toward it. But know where you are aiming.

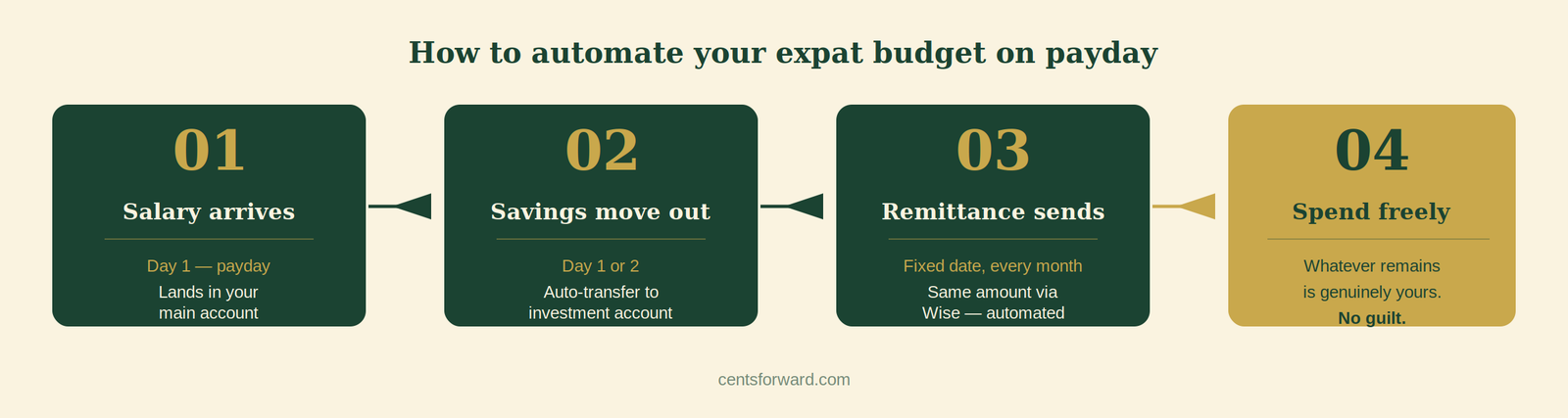

Step 4: Automate Before You Think

The biggest myth in personal finance is that the solution is discipline. It is not.

Discipline is a resource that depletes. Systems do not.

On the day your salary arrives, money should move automatically before your brain starts making spending decisions. This is not complicated. It is a transfer scheduled for the day after payday.

- Salary arrives in your main account

- Automatic transfer to savings or investment account within 24 to 48 hours

- Automatic remittance transfer on a fixed date (see Step 5)

- Whatever remains is your actual spending budget for the month

This single change inverts the default. Instead of saving what survives your spending, you spend what survives your saving.

Most people who try this report they do not even miss the money that moved automatically. It was gone before the decision could be made.

For moving money home quickly and cheaply, Wise is one of the most transparent options available to UAE residents. The mid-market exchange rate and low fees make it consistently better than a standard bank transfer.

Step 5: Budget Your Remittances Like Rent

This is the cost that silently destroys expat budgets more than any other.

Money sent home is not optional for most expats. It is a commitment as real as rent. But people treat it like a variable cost and feel blindsided every time it lands.

Pick a fixed amount. Pick a fixed date. Automate it. Stop making it a monthly decision.

The decision fatigue alone drains you. The guilt when you send less than expected. The pressure when your family assumes more is coming. The month-end scramble when you forgot to account for it.

All of that disappears when remittances become a fixed line, not a variable one.

If the amount feels unsustainable relative to your income, that is important information. It may mean a direct conversation with your family is overdue about what is genuinely manageable long-term.

That conversation is hard. It is also the financially honest move.

Step 6: Build a Guilt-Free Spending Category

Every budget that lasts has a release valve. Budgets that feel like permanent deprivation get abandoned.

This is not a weakness. It is just how humans work.

Once you have covered your needs, saved your 30%, and sent money home, what remains is genuinely yours. Spend it freely. No tracking required. No justification needed. You have already done the responsible part.

This category also protects the rest of your budget. When you know guilt-free spending exists inside your system, you stop making emergency exceptions everywhere else.

If you consistently run out before month end, that is a signal to review your fixed costs, not your self-control. The most common money mistakes that keep people stuck are rarely about discipline.

Step 7: Review Monthly, Adjust Quarterly

A budget is not a law. It is an educated first guess that gets more accurate over time.

Your first version will be wrong in at least two or three categories. That is expected and completely fine.

At the end of each month, spend 15 minutes on three questions:

- Did I hit my savings target? If not, what pulled from it?

- Which category ran over? Was it a one-off or is it a pattern?

- Did my actual income match what I expected?

Every quarter, run a bigger review. Look at three months of real data. Adjust your fixed cost assumptions. Update your exchange rate benchmarks. Raise your savings target if the numbers allow.

A good budget should become both more accurate and more ambitious over time — not sit frozen at your first draft.

Pair this with an annual check-in on your broader picture. The annual financial wellness check-up on CentsForward is a solid structure for that bigger review.

The Tools That Make This Stick

What is the best budgeting tool for someone learning how to budget on an expat salary?

Most budgeting apps are built for single-currency, single-country users. For expats managing money across two or more currencies, they break down quickly.

A simple Google Sheet with four columns — income, fixed costs, savings, spending — is genuinely all you need in the first three months. This is the foundation of how to budget on an expat salary without overcomplicating it.

Build the habit before building the system. Knowing how to budget on an expat salary is about consistency first, tools second. Once you are consistent, you can layer in more detailed tracking using one of the free spending tracker apps reviewed and ranked on CentsForward.

Should I keep savings in a separate account?

Always. Savings sitting in the same account as your spending money is invisible and therefore spendable.

A separate account creates a psychological barrier that works precisely because it adds one extra step between you and the temptation.

Once your emergency fund covers three to six months of fixed expenses, that money needs to start working for you. The emergency fund guide on CentsForward covers exactly what that baseline should look like before you move into investing.

For UAE residents ready to invest, eToro accepts UAE residents and gives you access to global ETFs and stocks without needing a US brokerage account. Open an account with eToro and start with whatever you can commit to monthly.

For the full step-by-step process, the how to start investing as an expat post covers it specifically for non-US investors.

There was a month where I earned more than I ever had and still felt broke by the 22nd. I sat down and actually mapped where it went. The answer was not one big thing. It was eleven small things that I had never given a name to. Giving every dollar a job before the month started was the only thing that actually changed the pattern. Not willpower. Not motivation. Just a list made on the 1st.

The One Thing to Take From This

The real goal when you finally nail how to budget on an expat salary is not to spend less. It is to know exactly where your money goes and make sure some of it is quietly building something for you — not just passing through your account on the way to somewhere else.

You are building a life across borders. That takes a system built for that reality.

Start with Step 1 this week. Just the number. Everything else follows from that.

Want the free Expat Budget Starter Sheet?

Subscribe to the CentsForward newsletter and get a simple budget template built specifically for expat salaries, remittances, and cross-border investing. No jargon. No judgment.

Frequently Asked Questions

How do I budget on an expat salary when my income varies each month?

Base your budget on the lowest reliable income you have received in the past six months.

Anything above that baseline gets swept directly to savings or investments the moment it arrives. This protects you from lifestyle inflation when a good month hits and gives you a stable floor during slower months.

How much of my expat salary should I be saving?

A minimum of 20%, and ideally 30% if you are serious about building wealth.

As an expat with no local pension accruing in your host country, your personal savings rate has to do work that institutional systems handle for employees elsewhere. 20% is a floor, not a ceiling.

Can I invest while still learning how to budget on an expat salary?

Yes. In fact, part of learning how to budget on an expat salary is building investing into the budget from day one — not treating it as something you do with whatever is left at month end.

Platforms like eToro accept UAE residents and allow you to invest in global ETFs from a few hundred dollars. Starting small and consistently beats waiting for perfect conditions. See the full guide on how to start investing as an expat for a complete breakdown.